February 2026: San Francisco Real Estate Insider

Good morning.

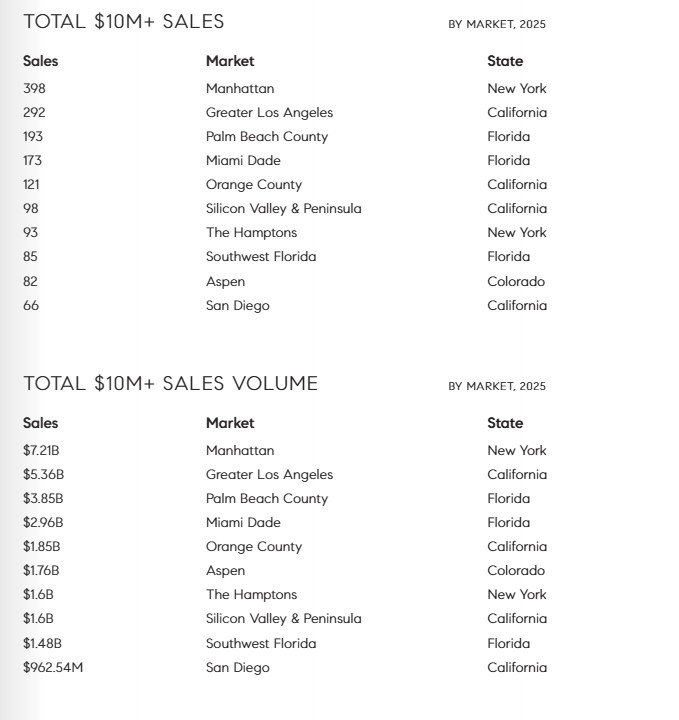

Now that we have 2025 in the rear view mirror and the full real estate sales data set to review, it appears San Francisco is not the only city / metro where the super luxury market is trending upward. Nationally, at $10M and above, 2025 was a year of broad re-acceleration. The top 10 ultra-luxury markets posted 1,601 sales totaling $28.6B – a 31% increase in transactions from 2024 and a 23% surge in volume.

The largest metro, Manhattan, had 30% more sales (than in 2024). Greater Los Angeles surged 54% (despite wildfires and mansion tax consternations). Palm Beach continued its post-pandemic streak with a 46% increase in sales.

The commonality is a broad expansion across coastal metros, resort destinations and emerging wealth hubs. Why have ultra-luxury homes outperformed the rest of housing? And more importantly, does this momentum appear durable?

Historically, ultra-luxury real estate has functioned as a lagging indicator of financial markets and liquidity events. Equity valuations, IPOs, mergers and acquisitions, and private funding rounds convert paper wealth into deployable capital. Viewed through that lens, continued growth at the top end of housing in 2025 is not surprising. So, at some point it will taper down, but that does not appear to be in the near term.

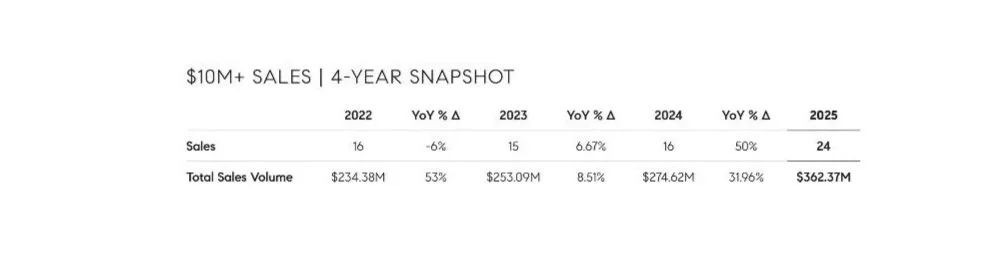

Back to San Francisco, our $10M sales are up 50% (YoY) and the driver continues to be AI wealth (and its ecosystem).

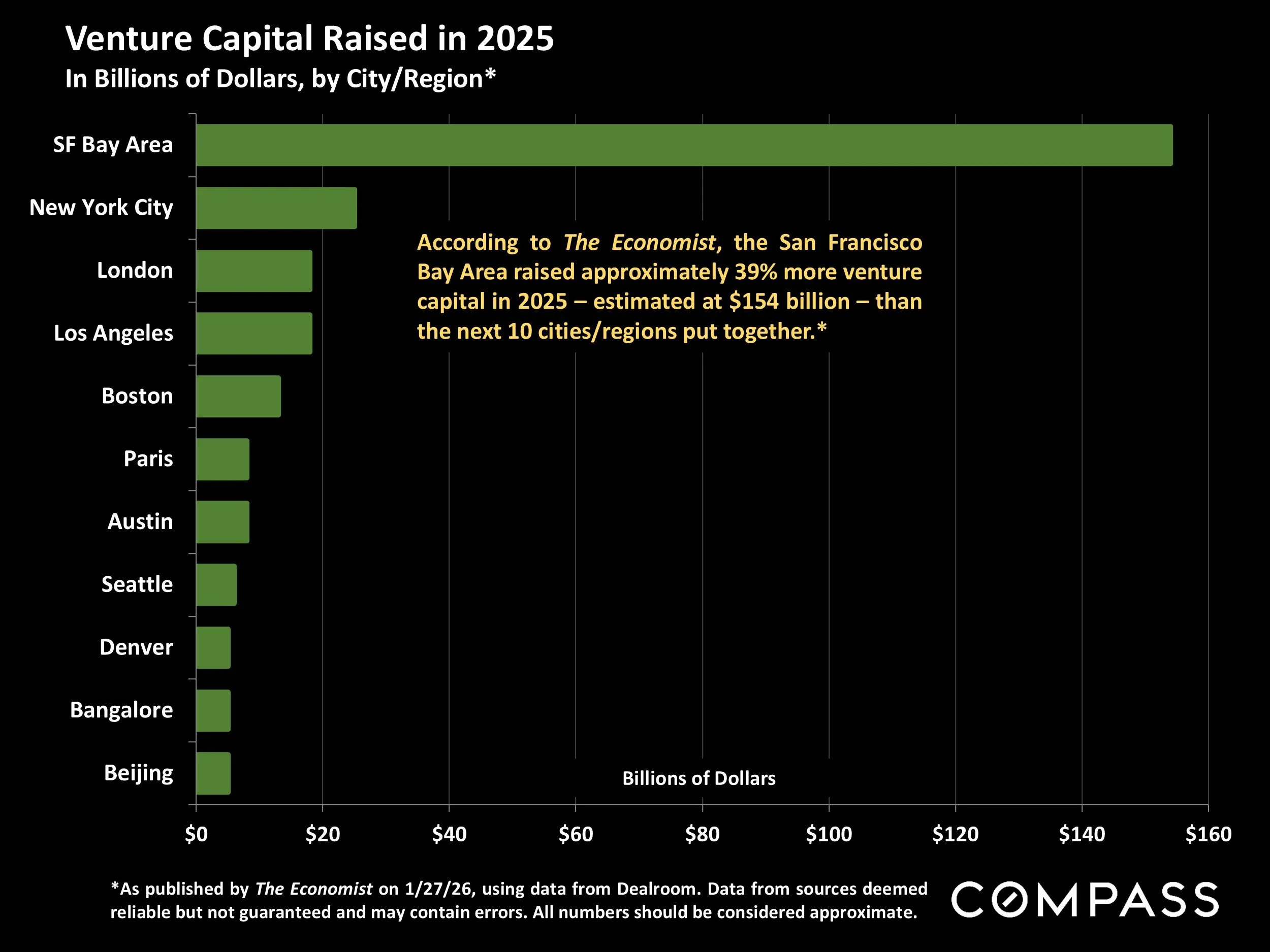

To give you an example of the disparity of venture capital investment in the Bay Area (for AI) versus other metro’s, the numbers are staggering: the Bay Area (and San Francisco as the “hub” for AI) companies received over $150B in venture capital investment in 2025. Companies in the second ranking city (New York City) received approx. $25B in investment.

This is driving the $10M+ sales boom.

Staying local, January did not start off as I expected with a flurry of new inventory attempting to jump the spring market. Instead, inventory is staying on the sidelines for the time being, yet the buyers are getting impatient. Hopefully this month we’ll see the inventory start to trickle onto the market.

The lack of inventory is also impacting the local off-market deal flow. More deals are happening without a property going to MLS than I’ve seen in some time. Again, with very little to purchase, discerning buyers are willing to “write the check” for exclusivity. Those quality properties that do go to market are seeing furious bidding wars. A couple examples of January bidding battles:

-1640 9th Avenue in the Inner Sunset. The home was listed for $2,495,000 and sold for $4,050,000.

-65 Carmelita off of Duboce Park. The home was listed for $4,398,000 and sold for $5,560,000.

That is it for now. I have a great 4BR/3.5BA Sea Cliff house with a Butler Armsden pedigree that I will start to show ASAP. If that fits your wheelhouse, please reach out.

Call or email, anytime.

About the Author

Scott Whelan provides San Francisco real estate sales and advisory services. His work centers on pricing strategy, market positioning, and identifying off-market opportunities.

For detailed comps, off-market opportunities, or a property-specific analysis, contact Scott Whelan directly.